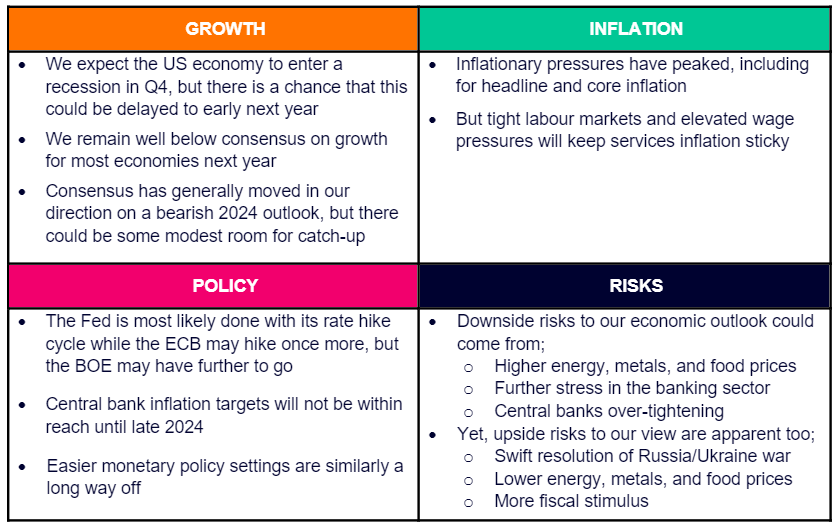

Despite near-term resilience, we expect a lacklustre economic outlook through 2024

Summarising this month’s investment view, Shweta Singh, Chief Economist at Cardano, commented: “Economic data in the US has been more resilient than expected, leading to upward revisions to the near-term growth outlook, but we think there is room for disappointment.

“Headline GDP figures from the last quarter mask the slowdown in private consumption and weakening domestic demand in general. Separately, the UK economy has also been more resilient, in line with our expectations. Meanwhile, the large downside data surprises in the Eurozone are in line with our view that too much optimism was baked into the Eurozone outlook. More importantly, beyond this year, consensus continues to move towards our long-held view that economic growth through 2024 will be tepid, including in the UK and across Europe.

“Financial conditions, which are crucial leading indicators of economic growth are tightening globally. The demand and supply of credit are deteriorating and the balance sheet support for households and business balance sheets is dwindling.

“The Federal Reserve is most likely done with its rate hike cycle while the European Central Bank may hike once more, but the Bank of England may have further to go. A structurally tight labour market and sticky wage growth will force central banks to keep the policy stance relatively tight through 2024.”

Core themes

Spotlight – Emerging Market Equities

We find Developed Market Equities unattractive at the moment and, whilst we are also cautious on Emerging Markets, we find better valuation and earnings prospects to be had in this asset class.

Developed Markets have rerated strongly through the past six months, led by the US and Japan. This has been justified by resilient growth and, for Japan, a weaker yen. However, we are concerned over how narrow market performance has been (see below). We expect weaker economic growth to weigh on earnings expectations and multiples from here.

Emerging markets earnings on the other hand look more realistic, valuations are more attractive. Fiscal stimulus and a weaker US dollar should also provide support.

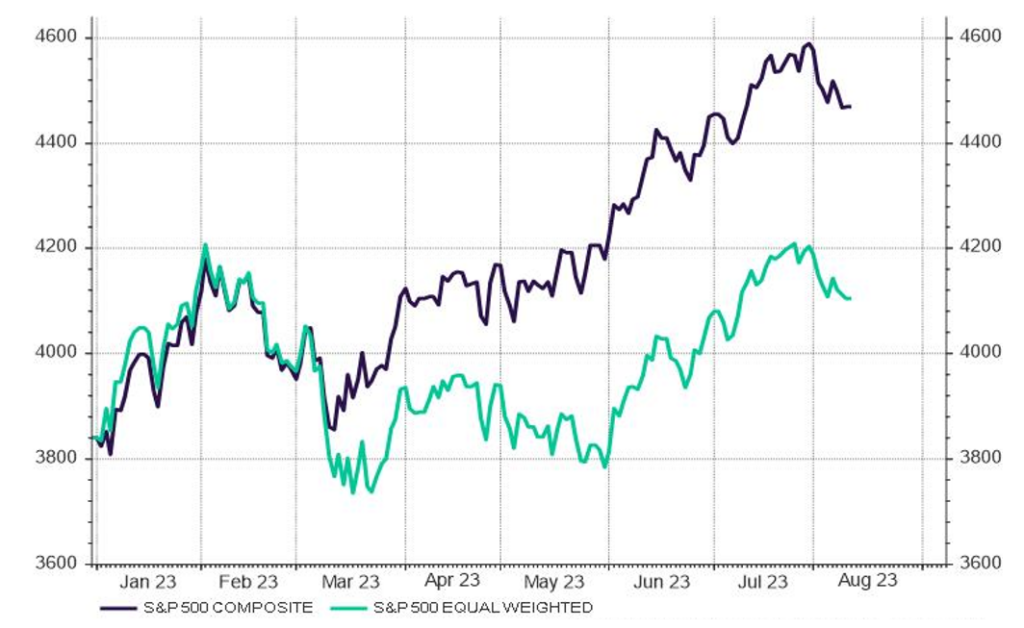

Chart of the month – The US equity market rally has been very narrow

Source: Refinitiv Datastream, Cardano

Why is this important?

- The graph compares the performance of the S&P500 (which is a market capitalisation weighted index) with an equally weighted index of the same constituent stocks.

- The comparison indicates how evenly the S&P500’s performance is spread amongst its constituents.

- When the comparison shows divergence, as has been the case since mid-Q1, market performance is said to be ‘narrow’. A ‘narrow’ market is one that is dominated by the returns of just a few constituents.

- Currently this dominance comes from the very positive performance of companies involved in Artificial Intelligence (AI) related sectors.

- Looking ahead, we are concerned that a reversal of sentiment in the AI sector will negatively impact overall market returns. The likelihood of seeing support from the long-tail of companies that have so far delivered modest returns this year appears to be low given our outlook for growth over the next several quarters.