Sustainability is at the heart of how we run our business. We believe we can contribute to the transition to a sustainable society – a fairer society with strong social foundations that operates within environmental boundaries: where people, businesses and nature can prosper, that offers a decent quality of life and provides financial security.

That’s why we view all our investment and advisory activities through a sustainability lens. Through sustainable investment, we aim to create better financial outcomes – as well as contribute to the transition to a sustainable society – and make our clients’ portfolios more resilient to an uncertain future. We provide sustainable solutions across investment advisory, investment management solutions and Defined Contribution pensions.

Working with pension scheme trustees and beneficiaries across the UK and Europe, our clients span industries, income levels, cultural and ethnic backgrounds, supporting young families to current retirees. The youngest members of these schemes may be over 50 years away from retirement or have young families that will live into the next century. What guides us is our belief that our clients’ members and their dependents should enjoy a quality of life similar to or better than what is possible today.

Exploring our key sustainability topics

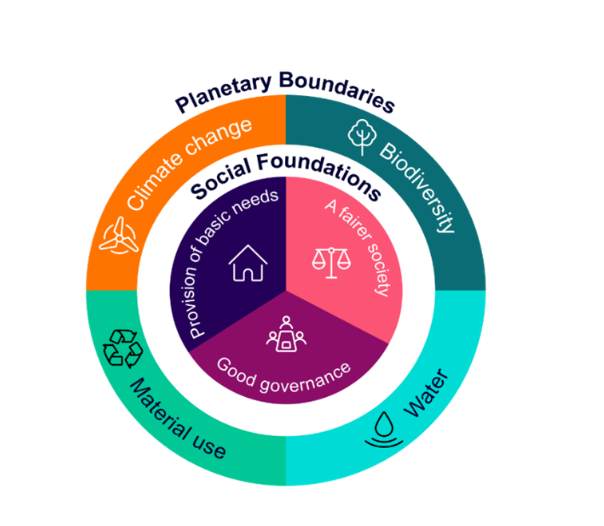

We’veidentified 4 environmental themes (planetary boundaries) and 3 social foundations that are crucial to support the transition to a sustainable society. Read more about:

Our biodiversity ambitions – biodiversity loss is a global systemic risk. Over half of GDP is directly or indirectly dependent on nature. We seek to understand where companies in our portfolios may be contributing to biodiversity loss throughdeforestation in their own activities or supply chains. Through innovative data and collaborative initiatives, weengage with companies, governments and regulators to address what is driving biodiversity loss and support net-zero deforestation by 2030. Learn more about our Biodiversity Strategy.

Our climate commitments – the climate crisis is one of the most fundamental challenges confronting the global economy. We support international goals to limit global warming to 1.5°C above pre-industrial levels. We’ve committed all our investment portfolios to net-zero carbon emissions by 2050, with ambitious interim targets. Our focus is on supporting the transition to net zero in the real economy, not only our investment portfolios. Read about our goals and plan to address climate change here.

Championing a fairer society – a fair society addresses inequality through access to education and training, income and work, paying a living wage, respecting labour rights and improving diversity and gender equality. Failure to do so increases systemic risks and leads to political and economic uncertainty, addressing these social foundations can improve the quantity and quality of economic growth. We engage with companies to encourage them to focus on these social foundations, and with governments and policy makers to develop supportive policies. Learn how we address social foundations here.

Exploring our key sustainability topics

We’veidentified 4 environmental themes (planetary boundaries) and 3 social foundations that are crucial to support the transition to a sustainable society. Read more about:

Our biodiversity ambitions – biodiversity loss is a global systemic risk. Over half of GDP is directly or indirectly dependent on nature. We seek to understand where companies in our portfolios may be contributing to biodiversity loss throughdeforestation in their own activities or supply chains. Through innovative data and collaborative initiatives, weengage with companies, governments and regulators to address what is driving biodiversity loss and support net-zero deforestation by 2030. Learn more about our Biodiversity Strategy.

Our climate commitments – the climate crisis is one of the most fundamental challenges confronting the global economy. We support international goals to limit global warming to 1.5°C above pre-industrial levels. We’ve committed all our investment portfolios to net-zero carbon emissions by 2050, with ambitious interim targets. Our focus is on supporting the transition to net zero in the real economy, not only our investment portfolios. Read about our goals and plan to address climate change here.

Championing a fairer society – a fair society addresses inequality through access to education and training, income and work, paying a living wage, respecting labour rights and improving diversity and gender equality. Failure to do so increases systemic risks and leads to political and economic uncertainty, addressing these social foundations can improve the quantity and quality of economic growth. We engage with companies to encourage them to focus on these social foundations, and with governments and policy makers to develop supportive policies. Learn how we address social foundations here.

Our approach to sustainable investments

Our investment beliefs drive our activities and outcomes for our clients. We focus our resources on driving change in areas that we are passionate about, where we are knowledgeable, and where we can have a real-world impact. We effectively stewardour clients’ assets andsupport the transition to address key social foundations and planetary boundaries.Read more about our investment beliefs and our approach to sustainable investments here.

Investing in the transition

We focus on supporting the transition to a sustainable society. Find out about Transition Investing here.